Due diligence happens every day, including in your daily life.

If you’ve ever applied to rent an apartment or applied for admission to university, then someone is doing due diligence on YOU. Indeed, when you are selecting among apartment buildings or universities, YOU are doing due diligence on which one is the best fit for you.

In the apartment example, the due diligence being done by the buyer (i.e., you) and the seller (i.e., the landlord) is primarily an exercise in “checking the boxes.” For the buyer, you ask if the rent fits into your budget, if the location is nice, and if the vacancy is available when you need it. For the seller, they ask if you, as a prospective tenant, have an adequate income, a clean financial and legal history, and can adhere to the pet policy of this building. We will broadly call this type of due diligence confirmatory due diligence.

In the university example, the due diligence takes on a much more strategic set of questions, none of which have simple yes/no answers. For the buyer (i.e. you), the set of questions you may ask are things like “what kind of jobs do graduates from this university typically take,” “what will be the impact on my career if I need student loans to afford this place,” and “what activities outside of class will I end up doing?” Sellers (i.e. university admissions departments) have a similar, if opaque, set of questions they ask themselves when determining the “fit” of each applicant. We will broadly call this type of due diligence exploratory due diligence.

The due diligence ecosystem we’ll discuss here has those same objectives. Investors have a plethora of options, and management teams running companies want to be selective about which investors they let participate in their capital structure.

Just like we gave two examples that featured both “buyers” and “sellers” of due diligence, we’ll look at who those players are in the investment world.

Who pays for due diligence?

In our introduction, we introduced private equity firms as being one of the largest consumers of due diligence, and we’ll talk shortly why they spend more per investment than any other type of investor.

But let’s remember that due diligence extends beyond just private equity. All institutional investors will conduct due diligence in one form or another. These include:

● Hedge funds;

● Mutual funds;

● Venture capital firms;

● Corporate M&A departments;

● Real estate investors.

The degree to which a firm might conduct due diligence varies dramatically according to their investment mandate (a fancy term for “investment strategy”).

Private equity (PE) and mutual funds, for example, tend to hold onto their investments for a relatively long period of time (5+ years), so they seek to collect every bit of knowledge they can that might influence the company’s future performance. The PE investor also intends to directly influence the company’s operations, whereas the mutual fund manager will most likely be a passive investor. Hence, due diligence for the PE investor must also account for prospective changes the PE investor intends to make.

They also tend to invest in fewer companies over that period of time, which means if one of their investments doesn’t provide returns, it’s very damaging to the health of the firm.

A venture capital fund, on the other hand, tends to employ a pray-and-spray approach, which means a lot of smaller investments in a large number of small companies with the assumption that some of them will fail. In this scenario, due diligence is limited for a few reasons:

1) The companies tend to be so small that the impact of financial due diligence is limited;

2) The success or failure of an investment is often based on the market more than the management team (we know this is a controversial statement and not always applicable);

3) The speed at which the companies a VC firm would invest in are growing at a rapid pace. Traditional due diligence, which may take months, is too slow to be useful for a VC firm;

4) The monetary cost of due diligence can be overwhelming. If a VC is putting $250k into a seed round, they aren’t going to hire KPMG for $100k to audit the startup’s books.

Who sells due diligence?

We’ve established that a firm’s investment mandate dictates how much appetite exists for due diligence. So who are the vendors who provide it?

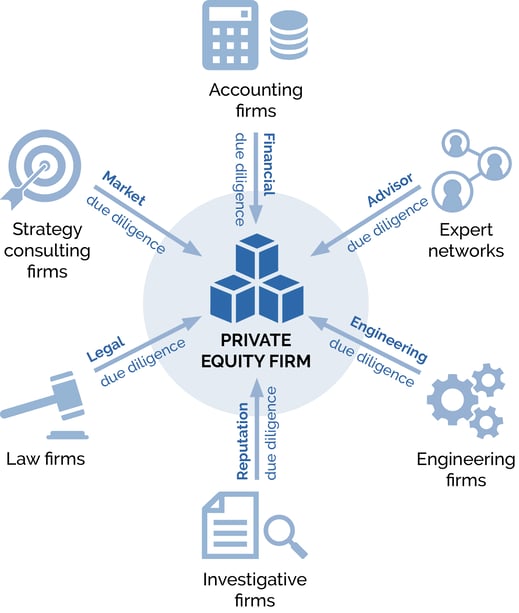

First of all, there is no one-stop-shop for due diligence. The industry has wisely chosen to respect certain boundaries such that accounting firms are specializing in accounting due diligence, strategy consulting firms are specializing in market due diligence, and so on. With a few exceptions, each player in the due diligence industry generally knows its role and sticks to it.

PE firms and corporate M&A departments are the two heaviest users of due diligence, so let’s look at the various streams of due diligence they will conduct.

Financial due diligence

An accounting firm will reverse-engineer financial statements and investigate any anomalies. This is almost always backwards-looking, and does not consider future financial projections. Typical vendors are the Big 4 accounting firms (E&Y, Deloitte, Ernst & Young, PwC), and the cost can be tens of thousands of dollars per week with 3-16 weeks needed.

Market due diligence

A strategy consulting firm will estimate the future growth of the market, often as defined as annual spend per year, as well as market share trends among existing & potential players. This is conducted typically by performing dozens of industry discussion calls and/or utilizing surveys.

Typical vendors are strategy consulting firms such as Bain, BCG, or McKinsey, and the cost is typically hundreds of thousands of dollars for a 3-6 week engagement. It is worth noting that there are some industry-specific consulting firms like IHS-CERA in the energy industry who may often do this work instead of a strategy consulting firm.

Additionally, some expert networks such as GLG and AlphaSights can be used to directly source experts to opine on market issues.

Legal due diligence

A law firm will review all of the key legal documents of a company, including (but not limited to) customer contracts, supplier contracts, employment agreements, stockholder agreements, and IP assignments.

Typical vendors are any major law firm. Fees can become enormous depending on the scope of the due diligence.

Engineering due diligence

An engineering or engineering consulting firm will be hired to perform one or all of the following:

-

Site analysis to ensure factories or installations of the target company’s product meet the targets set;

-

Feasibility analysis to ensure that projections of the company’s technology are reasonable.

Typical vendors vary significantly by industry and geography. Choosing who performs this due diligence is sensitive since, by definition, it involves the exposure of IP and key trade secrets to a third party.

Reputation due diligence

An investigative firm will perform background checks on management team members and occasionally investors or board members. The deliverable is a 10-100 page report per individual on this person’s financial and legal history as well as reference checks among peers and former colleagues of the individual. Typical vendors include Kroll, Blackpeak, and others. This exercise can cost at least a few thousand dollars per individual.

A final note on “doing” due diligence

What we’ve described so far is an oversimplification of who “does” due diligence. Reading the above, you would be forgiven for thinking that a PE firm, for example, pays for these various vendors to do due diligence. That is technically true, but the point we want to make is that it is ultimately the sponsor (i.e. the PE firm) who does the due diligence.

Within a PE firm, it is typically the Vice President on the deal team who coordinates all these streams of due diligence. So even though the PE firm may hire Bain and Kroll and KPMG and Cravath to “do” due diligence, we ultimately say that the PE firm is the one performing due diligence. The phrase “quarterbacking the deal” gets used often in American PE firms to refer to this process.

A reader should not conclude that PE firms (or any financial sponsor) outsource the process of due diligence. They hire multiple parties to answer specific questions, and then they report back the mosaic of results to the firm’s investment committee.

While due diligence comes in many shapes and sizes, the focus of the remainder of this guide will be on market due diligence, and more specifically on the due diligence services offered by expert networks. In the next chapter, we’ll unpack more specifically what these companies do and how you as an interpreter can dramatically enhance the value they offer to their clients.

Want the full guide?

Download your digital copy of the Interpreter's Guide to Industry Discussion Calls today!